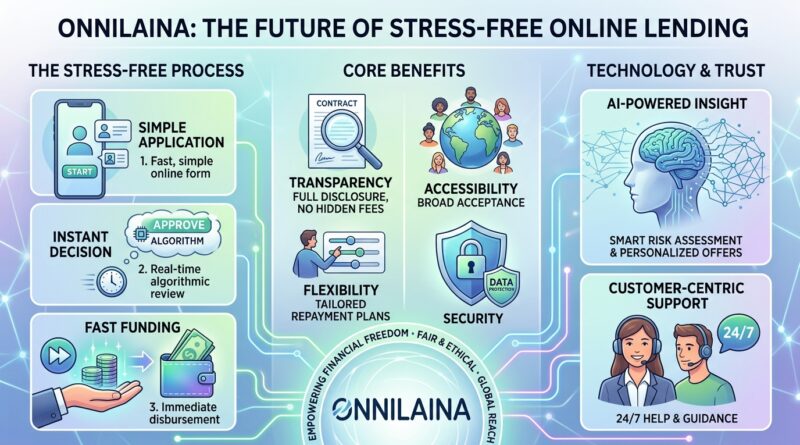

What is Onnilaina? The Future of Stress-Free Online Lending

Onnilaina is a modern conceptual term in digital finance that evokes “lucky” or “happy” borrowing. It combines Finnish roots “onni” for luck or happiness and “laina” for loan framing online lending as accessible, transparent, and low-stress rather than burdensome. In 2026, as consumers seek faster and more user-friendly financial tools, Onnilaina represents platforms and practices that prioritize simplicity, clear terms, quick decisions, and responsible borrowing in the online lending space.

This article explores the meaning, evolution, mechanics, categories, and implications of Onnilaina-style online lending for everyday users navigating personal finance in a digital world.

Why Onnilaina Matters in 2026

Digital lending continues to expand rapidly, with the global online consumer lending market expected to grow significantly amid demand for instant access to funds. Onnilaina-style services address pain points of traditional banking—lengthy approvals, opaque fees, and physical visits—by offering mobile-first applications, automated decisions, and transparent comparisons.

For users, this means reduced financial stress during unexpected expenses, home improvements, or cash flow gaps. The approach aligns with broader digital culture trends favoring convenience, control, and informed decision-making. In an era of economic uncertainty, services emphasizing clarity and responsibility help promote healthier borrowing habits while expanding access for underserved segments.

You might also like: Uprising

Evolution of Onnilaina

Early Days: Traditional Lending and Initial Digital Experiments

Online lending traces roots to the early 2000s with peer-to-peer platforms and basic web applications. Borrowers still faced manual reviews, paperwork uploads, and days-long waits. Early Finnish and European digital efforts focused on basic comparison sites, laying groundwork for faster processes but lacking the seamless, positive user experience now associated with Onnilaina.

Major Transitions: AI, Automation, and User-Centric Design

The 2010s brought mobile apps and instant pre-qualifications. By the mid-2020s, AI-driven credit assessments, open banking integrations, and regulatory sandboxes accelerated approvals to minutes. The term Onnilaina gained traction around 2025 as marketers and platforms highlighted “lucky loan” framing to reduce stigma. Post-pandemic shifts toward fully remote finance cemented its relevance, with emphasis on transparency amid rising consumer protection rules.

Onnilaina in the Broader Fintech Ecosystem

Onnilaina operates at the intersection of fintech innovation and consumer trust. Platforms leverage data analytics, machine learning for risk assessment, and API connections to banks for real-time verification. This ecosystem reduces costs for providers while delivering speed and choice to users. It reflects wider digital trends where technology simplifies complex services without sacrificing security or regulatory compliance.

Major Platforms Powering Onnilaina Experiences

Instant Personal Loan Apps

Mobile-first services offer quick applications with minimal documentation, using AI for instant decisions and fund disbursement within hours.

Loan Comparison Aggregators

These platforms allow one application to generate multiple offers from partner lenders, helping users compare rates and terms side-by-side.

Embedded Finance Solutions

Integrated into e-commerce or banking apps, these provide contextual lending options at the point of need, such as buy-now-pay-later extensions or small emergency loans.

Peer-to-Peer and Alternative Lenders

Modern P2P models with institutional backing provide competitive rates and flexible terms, often with stronger emphasis on responsible lending practices.

You might also like: Just Taking Up Space: A Review of Classical Conversations

Types of Onnilaina Lending Options

Short-Term Personal Loans

Designed for immediate needs, these feature fast approval and clear repayment schedules, ideal for bridging short cash gaps.

Installment and Flexible Loans

Longer-term options with predictable monthly payments, often including early repayment without penalties to support borrower control.

Secured vs. Unsecured Digital Loans

Unsecured versions rely on credit profiles for speed, while secured options use assets for better rates, with streamlined online collateral processes.

Specialized Niche Offerings

Categories include debt consolidation tools, education financing, or small business micro-loans, each tailored with user-friendly interfaces and educational resources.

Key Strategies for Safe and Effective Use

Pre-Application Assessment

Users should evaluate their budget, credit profile, and actual need before applying. Many platforms offer pre-qualification tools that don’t impact scores.

Comparison and Due Diligence

Always review total cost of credit (APR, fees, total repayment) across offers rather than focusing solely on monthly payments.

Responsible Borrowing Practices

Borrow only what can be repaid comfortably and utilize built-in tools like calculators or financial literacy resources provided by quality platforms.

You might also like: Uffufucu6: How AI and Automation Are Leading the Trend

Tools, Technology, and Application Processes

Modern Onnilaina workflows use secure digital ID verification, open banking for income/expense insights, and AI for rapid risk scoring. Applications typically involve basic personal details, consent for data pulls, and instant or near-instant offers. Backend automation handles compliance checks, while user dashboards provide repayment tracking and support chatbots. Security features like encryption and two-factor authentication are standard.

Monetization and Business Models (for Providers)

Platforms earn through interest spreads, origination fees, partnership commissions, or premium features. Successful models balance profitability with responsible practices to maintain regulatory approval and user trust. Data insights also inform ancillary services like insurance or savings tools.

Challenges and Criticisms

Despite benefits, risks include high effective costs for lower-credit users, potential for impulsive borrowing due to ease, and data privacy concerns. Regulatory scrutiny varies by region, and not all platforms maintain equal transparency. Critics note that speed can sometimes overshadow long-term affordability education. Balanced perspectives emphasize the need for strong consumer protections alongside innovation.

Future Outlook

Advancements in AI personalization, blockchain for secure records, and tighter integration with everyday banking apps will likely enhance Onnilaina experiences. Greater regulatory harmonization and focus on financial inclusion could expand access while addressing risks. The core promise—stress-free, transparent lending—will remain central as digital finance matures.

Conclusion

Onnilaina symbolizes a shift toward lending experiences that feel empowering rather than intimidating. By combining technological efficiency with user-centric design and transparency, these services offer practical solutions for modern financial needs. For individuals, the key is informed engagement: understand terms, borrow responsibly, and use tools as aids to financial stability. As digital lending evolves, Onnilaina-style approaches provide a promising framework for accessible, low-stress borrowing in 2026 and beyond.

FAQs

What does Onnilaina actually mean?

It blends Finnish words for “luck/happiness” and “loan,” representing positive, stress-free online borrowing experiences.

Is Onnilaina a specific company or a general concept?

Primarily a conceptual term for user-friendly digital lending practices and platforms emphasizing transparency and convenience.

How safe are Onnilaina-style online loans?

Safe when using regulated, transparent providers. Always verify licensing, read full terms, and check reviews.

Can anyone qualify for these loans?

Eligibility varies by income, credit history, and local regulations. Pre-qualification tools help assess chances without credit impact.

How does it differ from traditional bank loans?

Faster approvals, more digital convenience, and often broader accessibility, though rates and terms should still be compared carefully.

Disclaimer: The information shared on this website is intended for general informational use only. Accuracy and timeliness are not guaranteed, so readers are encouraged to independently confirm any important details before relying on the content.

Disclaimer: The content provided on this website is for general informational purposes only. While efforts are made to keep the information accurate and up to date, no guarantees are given regarding its completeness or reliability. Readers should verify any important information independently before making decisions based on the content.